Canada Post just reported the worst year in its history. It's also telling Ottawa that won't be enough.

The Crown corporation posted a $1.57 billion pre-tax loss for 2025. That's its biggest ever. It's surviving on $2 billion of federal loans, roughly split between a $1.03 billion package approved last year and another $1.01 billion approved in early 2026. Both are supposed to be repaid. Nobody inside the company believes that's realistic on the current trajectory.

Where The Losses Came From

Parcel volumes dropped by 79 million pieces last year. That alone translated to $850 million in lost revenue. Canada Post blamed strike action and private carrier competition.

Amazon and other retailers shifted more Canadian last-mile delivery to private carriers during the 2024-2025 labour uncertainty. Once those contracts moved, they haven't come back. Customers rarely do.

Think of the postal service as a grocery store that lost its biggest buyer. The lights stay on. The bills don't.

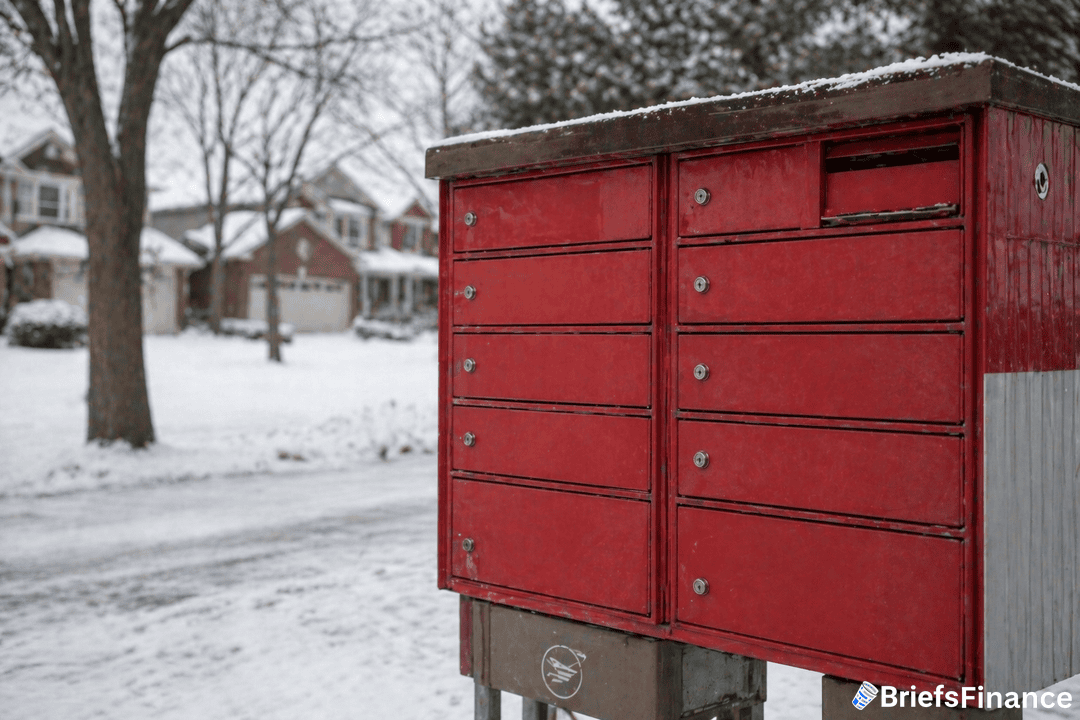

The Fix Is A Mailbox

Canada Post is planning to end doorstep delivery for the 4 million addresses that still have it. Those customers will get assigned to community mailbox clusters over the next five years. The company says that move alone saves $400 million a year.

That's a quarter of the 2025 loss, recovered by cutting the thing that most Canadians associate with mail service. The political fight will be loud. Rural residents, elderly Canadians, and accessibility advocates have already pushed back. The math isn't really in question. The politics is.

The Mailbox Fight Already Brewing

The community mailbox rollout is set to run over five years, which gives opponents plenty of time to turn it into an election issue. Rural MPs are already raising the accessibility angle, arguing that elderly Canadians and people with mobility issues can't walk to a cluster box in a Manitoba winter.

Accessibility groups have filed formal objections with Canada Post's regulator, which pushes the timeline longer and adds legal costs on top of the delivery savings.

The underlying business math doesn't change while the politics plays out. Parcel volume that moved to private carriers during the 2024-2025 strike uncertainty is not coming back, which means the $850 million in lost revenue is baked in whether the mailbox plan clears the fight or not.

Think of Canada Post's problem as a store that lost its anchor tenant. You can cut staff. You can change the sign. You can renegotiate the lease. The foot traffic that left does not walk back in because you did any of it.

Worth Noting

Canada's post office is not alone. The US Postal Service has lost money for 17 of the last 18 years. Royal Mail is privatising. Deutsche Post has leaned into logistics and away from letters.

Government-run mail services built for letters are trying to survive in a world where the parcel business has already been taken by private couriers. Canada Post's story is what happens when that transition stalls.

The loans bought Canada Post a year. The mailbox plan has to buy it the next decade.