Retail sales look hot. Then you look under the hood.

March retail sales climbed 1.7% from February. That's the biggest monthly jump in more than three years. Year over year, Americans spent 4% more than they did last March.

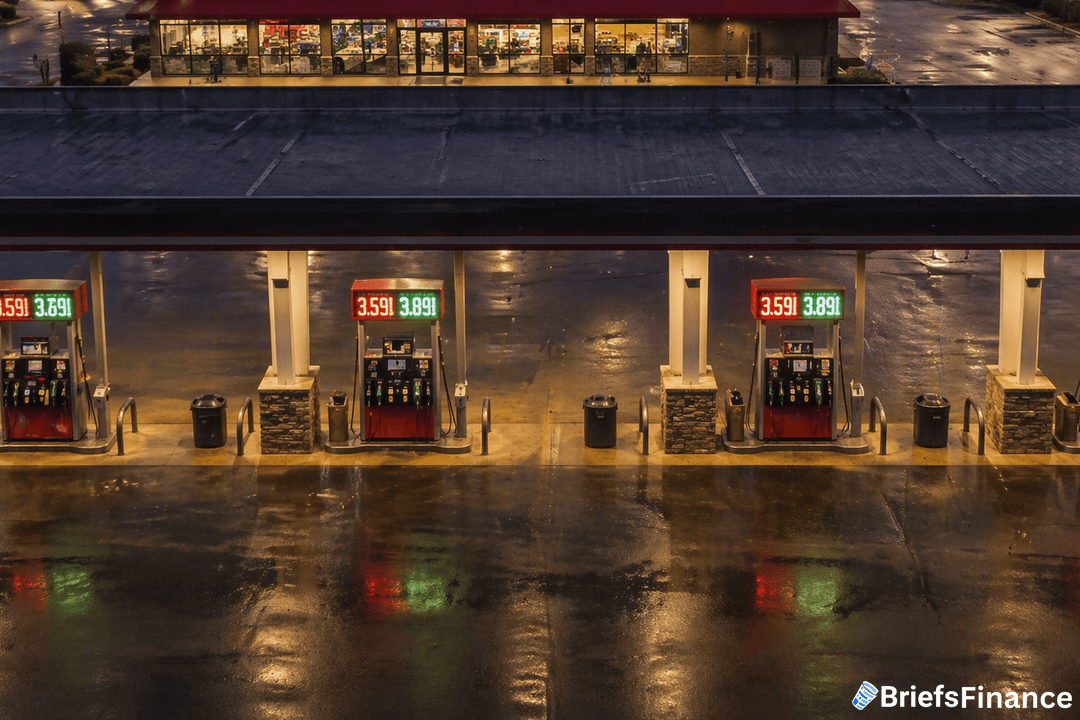

Here's the catch. Gas station receipts ran up 15.5% on their own. Gas prices climbed 24.1% in the same window thanks to the US-Israel war with Iran. When crude jumps 30%, gas receipts go with it. People aren't buying more fuel. They're paying more for the same tank.

What The Core Number Says

Strip out cars, gas, and building materials and you get a cleaner read. That retail control group rose 0.7% in March, against a 0.2% forecast.

The gains were spread across electronics, furniture, and general merchandise. Motor vehicle sales also rose. Spring tax refunds helped too, giving shoppers a one-time bump in walking-around money.

In other words: even after you scrub out the oil shock, people are still buying.

Why That Matters Right Now

Investors have been arguing about whether the US consumer is breaking. This report pushes the answer toward "not yet." Jobs are holding up. Wages are still rising. And the core retail number just came in three times hotter than economists expected.

Think of retail sales as the heartbeat of the economy. The Iran war is a fever running through the reading. Core sales show the heartbeat underneath is still steady.

The Atlanta Fed's GDP tracker will likely tick higher on the back of this number. That complicates the rate-cut debate the Fed is about to walk into.

Where The Dollars Actually Went

Motor vehicle sales rose in March, which matters because cars are a big-ticket buy that usually slows first when consumers get nervous. Electronics and furniture both climbed too, with general merchandise pulling its weight on top of that.

Part of the March lift was tax refund timing. Refund checks landed early for a chunk of filers this year, which tends to push electronics and furniture higher as households spend the windfall on things they've been delaying.

The broad-based gains are the cleanest read. When only one category carries a month, it's a promo or a weather story. When four categories move together, it's a consumer still showing up at the register.

Electronics and furniture moving together usually points to households that feel stable enough to swap out a TV or a couch. Motor vehicles rising alongside says the same thing with a bigger price tag attached.

General merchandise is the quieter tell. That line covers everyday store spend at big-box and department names, which moves with everyday confidence more than it moves with one-off promos.

Taken together, those four categories cover the bulk of discretionary retail. When all four move up in the same month, it's consumer strength showing up in the actual receipts.

Worth Noting

March was strong. April is a different story. Consumer confidence is weaker. Oil is still bouncing around on headlines out of Iran. Goods moving through ports are more expensive thanks to tariffs.

One good month doesn't settle the argument. It pushes it into May.