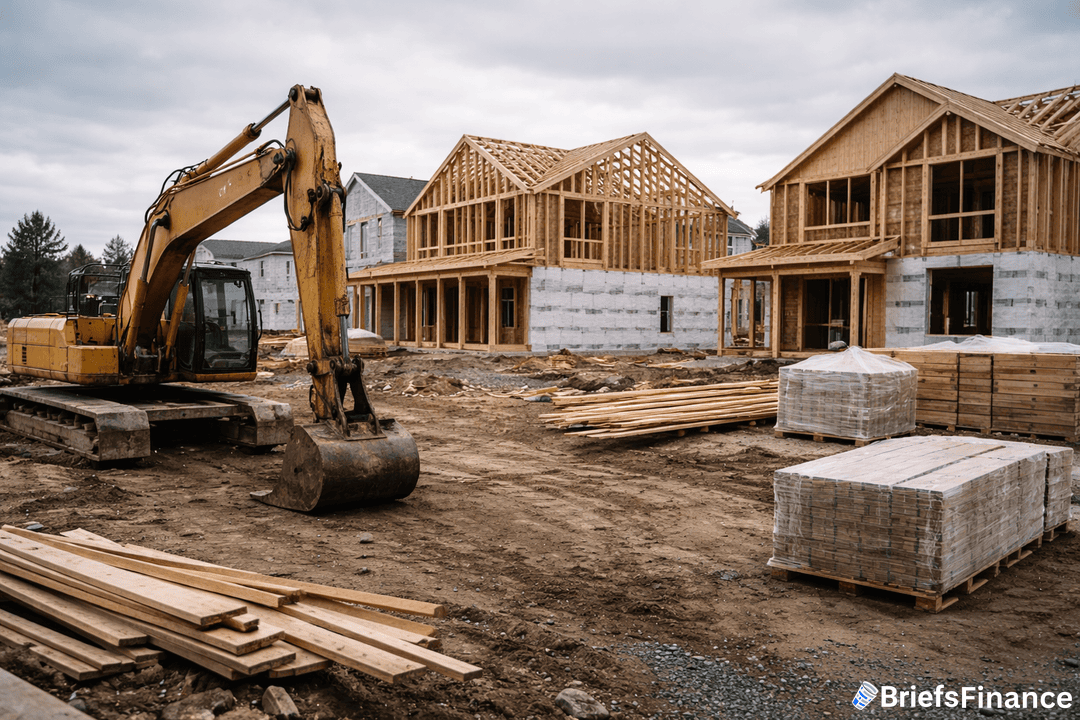

Single-family build-to-rent housing starts plunged 19% from 84,000 units in 2024 to 68,000 in 2025 as developers face higher financing costs and political pressure. Policy proposals could eliminate 40,000 potential units annually if rules tightening institutional ownership pass, with residential construction declining across all sectors as higher costs and regulatory constraints pile on the industry.

Politics Rewrites the Development Playbook

Lawmakers are discussing rules that would limit how many single-family homes institutional investors can own in a given market area, creating massive uncertainty for anyone planning projects years in advance. Some proposals could eliminate 40,000 units per year from the pipeline, which is staggering when the U.S. needs millions of new homes, as developers don't know whether to keep building for investors or pivot to other strategies entirely.

Rent Growth Cooling Despite Supply Shortage

Rents are barely rising anymore despite the housing shortage deepening across the nation, as U.S. single-family rents climbed just 1.2% year-over-year in December 2025, down sharply from 2.5% prior year. That's a serious problem for anyone banking on strong rental income to justify capital invested, as weak rent growth means returns don't justify the risk, and construction is slowing across residential, industrial, retail, and senior housing simultaneously.

The Supply Crisis Deepens

This slowdown is deeply concerning because the U.S. faces a severe housing shortage that requires both rental units and ownership opportunities to meet demand. When institutional builders step back due to policy uncertainty, nobody fills that gap at scale, and single-family rentals often provide cheaper options than ownership, so removing supply hurts affordability rather than helping it.

What to Watch

If policy restrictions on institutional ownership pass, housing affordability will likely get worse because rental units from big operators are often cheaper than single-family purchases.